Not long ago I came across a Tik Tok video of a mother sharing some life skills with her children. I was impressed because two of them looked to only be tweens, while the other ones weren’t more than seven or eight years old. She had assigned them a budgeting project where they had to figure out how they would be able to afford living out on their own. I thought it was a one-off video clip, until others showed up in my feed, so I began following her.

The first one had the daughter trying to figure out if she could afford the average rent in her area. You could see and hear her frustration as she realized how much of her paycheck would go towards just having a place to live. The next one I came across was a clip of the two older ones learning the hard reality of buying and maintaining a car and making payments; even for used vehicles. With smart phones in hand, the kids checked the cost of reliable transportation. One went from researching a 2015 vehicle to a 2010, in order to save more money. A third clip was one of the cutest, when one daughter indicated she would need to skip breakfast and lunch, and only eat dinner, just so she could afford all of her bills. In that clip, another one said she planned to buy a van and then live out of it to save on rent. Of course, she’s not thinking about where she plans to shower, use the restroom facilities, get dressed, or the cost of parking the van somewhere when not at work. One funny moment was when one of the girls seemed to get frustrated that her brother had $11 left over in his budget, when she ended up broke.

It was interesting to watch. And the exercise itself is similar to homework I assign my college students in a career readiness class I teach. I think teaching these kinds of financial life skills to kids, teenagers and young adults is so important so that they have a realistic viewpoint of the work world and adult responsibilities. But it’s not happening like it used to, and there’s a debate over why.

Many adults point their finger at the school systems for dropping the ball in this area and letting kids down. When I was a young teen, courses like Home Economics were taught in school where we learned simple budgeting practices, and other life skills stuff like that. Of course, that was several decades ago, before many states started cutting public school funding, and school boards decided that life-skills courses weren’t as important as core classes, such as English, Math and Science. As such, we’ve raised two generations, since my days, who were never taught many of the basic concepts of finances and financial responsibility.

But before we lay blame only with the schools, another notable change over the past 25-30 years seems to be a growing lack of involvement and responsibility of parents to teach their own children about money, making a budget, how credit works, and the basic principles of understanding the cost of living, and living within one’s means. A lot of parents don’t like to hear this, as witnessed by how defensive I’ve seen many of them become (strangers online, and friends and family I personally know), when this subject comes up. But think about it. If the under 40 generations don’t understand things like how federal and state taxes work, the difference between gross and net income, the impact of interest rates on credit cards, car payments, and mortgages, or how to create a budget based upon their take-home pay, then who’s fault is it? Where should they be learning about this if not at home; hopefully modeled by the actions of their own parents.

I think that’s why I found those video clips so impressive. Sure, the mother may have just been trying to create content for Tik Toks to feed her accounts. But it certainly seemed to be about more than that. She was starting them young and educating them early. She gave them real life situations to work through — rent, transportation, groceries, taxes — and then helped them see the big picture of what it takes to afford a living away from her home.

In America, we seem to be living in a time when people, not just the 20-something and 30-something crowd, but their parents as well, want to only put the blame for their financial struggles on inflation, the growing housing and rental market, and the overall higher costs of living. And yes, all of these things factor into the challenges we face in today’s economy. But what is our objective and ultimate responsibility to helping the young adults in our lives to learn and grow during this time? After all, if you’re over 40, you’ve been through it before — perhaps as a teenager in the 1980s, a college student or young adult during the crash of 1989 and the early 90s; or as a working adult when the big recession of 2008 hit, which took the economy over four years to recover, but not before many people lost their jobs, their homes, their cars, and their healthcare.

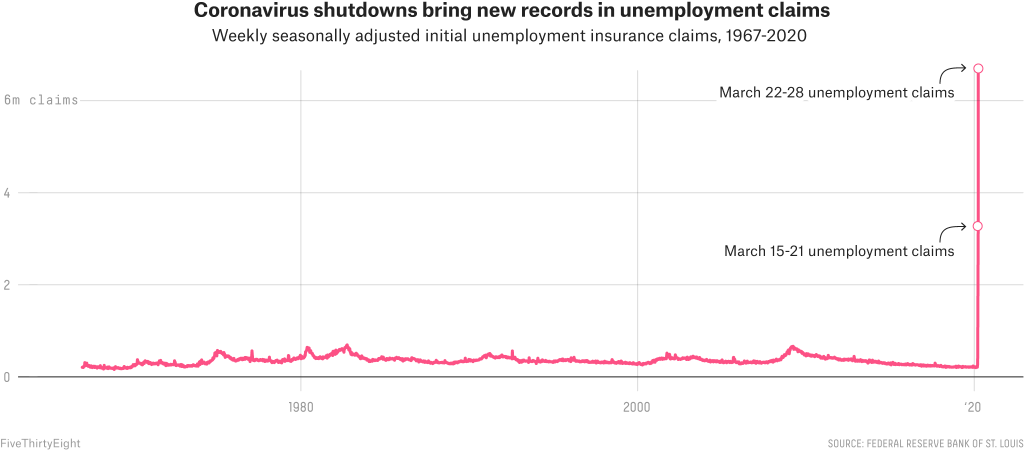

And now, we are living in this post-pandemic time. There’s a new generation living through a new economic challenge.

What did WE learn from our survival experiences that we should be teaching our college-aged and young adult children so that they not only know how to get through this, but also come away from it having learned how to help their own children do the same. Inflation and recessions are cyclical. So, it’s not a matter of IF but WHEN another one happens.

If our objective is simply to provide them with a free place to live, food to eat, help with their bills, and medical coverage on our insurance plans, then we are doing them a great disservice.

We need to be teaching them how to handle their money. How to save for emergencies and invest for the future. We need to not be afraid of talking to them about their spending habits and show them how to create and stay on a budget.

It does no good for parents to simply cover their adult children while at home, and then expect them to go out into the world and know how to make adult decisions with their finances in their own space later. They may not ask for it now. But that doesn’t mean they don’t need it. After all, to use a sentiment our parents often repeated to us, they are still living under your roof.

99.999 percent of you will never win the million dollar lottery. And almost as many will likely never receive a multi-hundred thousand dollar settlement or inheritance. So the reality is that if you are living with debt that you can’t pay off each month, and you want to change that, then you have to be willing to change you. And by changing you, I mean, change your mindset about debt.

99.999 percent of you will never win the million dollar lottery. And almost as many will likely never receive a multi-hundred thousand dollar settlement or inheritance. So the reality is that if you are living with debt that you can’t pay off each month, and you want to change that, then you have to be willing to change you. And by changing you, I mean, change your mindset about debt.